IRS COVID Refund Deadline: Protect Your Penalty Claim Before July 2026

In November 2025, the U.S. Court of Federal Claims issued a ruling in Kwong v. United States that could wipe out certain pandemic-era tax penalties. The National Taxpayer Advocate estimates tens of millions of taxpayers might be eligible for relief.

However, the IRS is actively fighting the decision. Because the agency is expected to appeal, no automatic checks are going out. To protect your right to a potential refund, you must mail a physical “Protective Refund Claim” before the strict deadline.

The IRS COVID refund deadline is July 10, 2026. Under the Kwong v. United States ruling, taxpayers who paid failure-to-file or failure-to-pay penalties between January 2020 and July 2023 may be eligible for a refund. To qualify, you must mail a paper “Protective Refund Claim” using IRS Form 843.

Key Takeaways

- The Kwong v. United States ruling effectively paused federal tax filing and payment deadlines from January 20, 2020, through July 10, 2023.

- The relief broadly covers tax penalties assessed for tax years 2019, 2020, 2021, and 2022.

- The Department of Justice is appealing the decision, meaning the IRS will not issue these refunds automatically.

- You must file a protective claim by July 10, 2026, to keep your statute of limitations open.

- The IRS requires you to file this claim via paper mail using Form 843.

- The National Taxpayer Advocate recommends sending your form via USPS Certified Mail with a return receipt.

Quick Start Guide

If you believe you qualify, do not wait for the IRS to send a letter. Download IRS Form 843 directly from the official agency website. Write “Protective Refund Claim Pursuant to Kwong Case” across the top margin and prepare to mail it via certified mail. Consult a tax professional to review your specific account transcripts before sending.

What is the Kwong v. United States Ruling?

In late 2025, the U.S. Court of Federal Claims delivered a significant decision regarding how the IRS handled tax deadlines during the pandemic. The court looked at the disaster-relief provision found in Internal Revenue Code Section 7508A(d).

According to the ruling, the IRS should not have assessed failure-to-file penalties, failure-to-pay penalties, or certain interest during the height of the COVID-19 emergency.

The “Disregarded Period” Timeline

The court determined that the federal disaster declaration effectively paused tax deadlines for roughly three and a half years. The COVID-19 federal disaster period ran from January 20, 2020, through May 11, 2023.

This means returns and payments were not legally late under the ruling until after July 10, 2023. This block of time is known as a “disregarded period.”

Confirmed vs. Unconfirmed Matrix

| The Kwong Case Element | Current Status | What It Means for Taxpayers |

| Court Decision | Confirmed | Penalties were improperly assessed during the disregarded period. |

| Automatic Refunds | Unconfirmed | The IRS is not issuing checks on its own. You must ask for it. |

| DOJ Appeal | Confirmed | The government is fighting the ruling in higher courts. |

| The Protective Claim | Confirmed | Filing Form 843 freezes your legal deadline while the appeal plays out. |

Who Qualifies for the COVID-Era Penalty Refund?

The ruling does not just apply to a single group of people. Affected entities include individual taxpayers, small businesses, corporations, estates, trusts, and U.S. expats.

If you paid a penalty for filing late or paying late during the disregarded period, you fall under the umbrella of this decision.

Targeted Tax Years: 2019 to 2022

The relief covers tax returns whose original deadlines fell inside the pandemic pause. This primarily involves tax years 2019, 2020, 2021, and 2022.

The IRS has offered limited penalty forgiveness in the past. In 2022, the IRS previously issued Notice 2022-36, which provided automatic relief for certain 2019 and 2020 returns. The Kwong case expands significantly upon that period. It also covers failure-to-pay penalties, which Notice 2022-36 largely ignored.

Eligibility Quick-Check Matrix

| Qualification Criteria | Eligible | Not Eligible |

| Entity Type | Individuals, Businesses, Trusts, Estates | N/A |

| Tax Years Covered | 2019, 2020, 2021, 2022 | 2018 or earlier; 2023 or later |

| Penalty Type | Failure-to-File, Failure-to-Pay, related interest | Accuracy-related penalties, fraud penalties |

| Original Deadline | Fell between Jan 20, 2020, and July 10, 2023 | Fell outside the disregarded window |

Typical Scenario Example: An individual taxpayer filed their 2020 tax return late and was assessed a $1,500 failure-to-file penalty. Under the Kwong ruling, the deadline was theoretically paused. By filing Form 843 before July 10, 2026, they protect their right to recoup that $1,500 if the Department of Justice’s appeal fails.

Common Mistake: Assuming your CPA automatically filed this for you. Unless you specifically signed a new Form 843 explicitly citing the Kwong case, your statute of limitations is not protected.

Why the IRS COVID Refund is Not Automatic

The U.S. government does not agree with the Court of Federal Claims. The Department of Justice and the IRS expect to appeal the ruling to a higher court. Because the case is actively disputed, the IRS is not voluntarily adjusting accounts or mailing checks to taxpayers.

Despite the pushback, the scope of the ruling is massive. As the National Taxpayer Advocate, Erin Collins, noted: “This issue is widespread and not limited to a small or specialized group of taxpayers.”

The Importance of the “Protective Refund Claim”

Federal law strictly limits how much time you have to claim a tax refund—this is called the statute of limitations. For a 2020 tax penalty, that window normally closes within a few years. If you wait to see if the IRS loses its appeal, your legal window to claim the money will likely expire.

A protective claim is exactly what it sounds like. It acts as a legal placeholder, freezing your statute of limitations while the courts settle the dispute.

Regarding the urgency of the deadline, Collins warned: “Unless the IRS or Congress acts… taxpayers seeking refunds… will, in most cases, need to file claims by July 10, 2026.”

Pro Tip: Never assume the refund is automatic or that the IRS will issue widespread waivers later. You must proactively file the paperwork to pause the statute of limitations on your account.

Mid-Article Summary Box

- The court ruled that pandemic-era tax penalties were improperly assessed.

- The IRS and the Department of Justice are appealing the decision.

- The IRS will not issue refunds without a formal request.

- You must file IRS Form 843 to freeze your statute of limitations.

- The hard deadline to mail this protective claim is July 10, 2026.

How to File a Protective Refund Claim (Form 843)

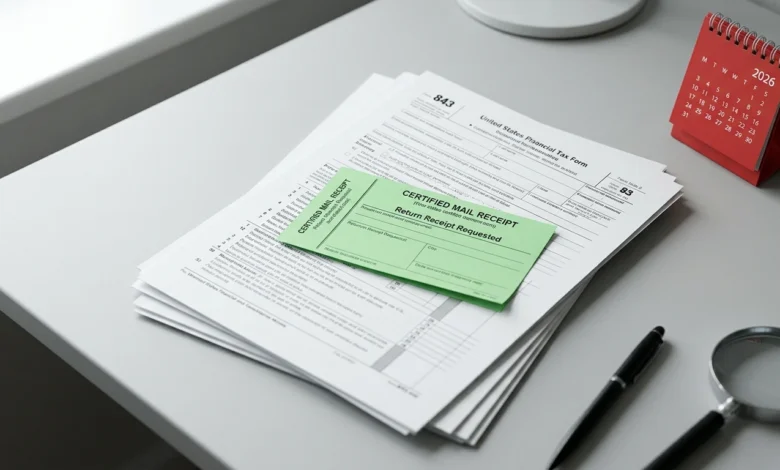

You must file this specific request on paper. There is currently no electronic filing option for a protective claim regarding the Kwong case. You will need to download and print IRS Form 843 Official Download and mail it to the designated IRS service center for your state.

Form 843 Mailing Safety Protocol

Because the IRS is handling millions of paper documents, creating an undeniable paper trail is your highest priority. Follow these steps carefully:

- Step 1: Mark the Contingency. Write “Protective Refund Claim Pursuant to Kwong Case” explicitly across the top margin of Form 843 in red or black ink. This tells the IRS processing clerk exactly why the form is being filed, even if it looks late by normal standards.

- Step 2: State the Reason. In line 7 of the form, clearly state that you are filing a protective claim based on the Kwong v. United States decision and are requesting the abatement of failure-to-file or failure-to-pay penalties during the disregarded period.

- Step 3: Track the Mail. Do not use standard postage. Send your envelope exclusively via USPS Certified Mail with a Return Receipt requested. The green receipt card with the postal stamp is your legal proof that you met the July 10, 2026 deadline.

Common Mistakes to Avoid When Claiming the Penalty Refund

Because paper forms require manual processing, small errors can lead to automatic rejections. Avoid these frequent missteps:

- Combining tax years: You cannot bundle multiple years onto a single piece of paper. You must file a separate, distinct Form 843 for every individual tax year you are claiming.

- Filing without checking transcripts: Do not guess the penalty amounts. You need to pull your official IRS “Account Transcript” to verify exactly how much you were charged in failure-to-file or failure-to-pay penalties.

- Forgetting the signature: An unsigned tax form is legally invalid. Ensure you sign and date the bottom of Form 843 before sealing the envelope.

- Waiting for your CPA to do it automatically: Many taxpayers assume their accountant is handling this. Unless you signed a new, physical Form 843 recently, your claim has not been filed.

Typical Scenario Example (Small Business): A small retail business paid $4,000 in failure-to-pay penalties and interest for tax year 2021. Even though the Department of Justice is appealing the ruling, the business’s accountant prepares a protective Form 843 and sends it via certified mail. This action freezes the statute of limitations. If the IRS is forced to concede the case in 2027, the business is legally in line to get its $4,000 back.

What to Do Next

If you believe you paid penalties between January 2020 and July 2023, take action now. Do not wait until the summer of 2026 when tax professionals are overwhelmed.

Taxpayers are strongly advised to consult a qualified tax professional. A CPA or Enrolled Agent can review your specific account transcripts, verify your eligibility under the disaster-relief provision, and prepare the protective claim correctly.

End Summary

The Kwong v. United States ruling offers a rare opportunity to recover penalty fees assessed during the COVID-19 pandemic. However, the IRS will not hand this money back voluntarily. To protect your legal right to a refund while the government appeals the case, you must file a paper Form 843 before the July 10, 2026 deadline.

Next Steps:

- Log into your IRS online account and download your “Account Transcripts” for tax years 2019 through 2022.

- Review the transcripts for failure-to-file or failure-to-pay penalty codes.

- Contact a tax professional to prepare and mail your protective Form 843 via USPS Certified Mail.

FAQs

Is the IRS COVID penalty refund guaranteed?

No. The IRS and the Department of Justice are appealing the Kwong v. United States decision. Filing a protective claim simply preserves your right to get a refund if the government loses its appeal.

Can I file Form 843 electronically for the Kwong case?

No. Currently, the IRS requires Form 843 to be filed via paper mail. There is no e-file option for this specific protective refund claim.

What tax years are covered by the Kwong ruling?

The ruling covers penalties assessed during a “disregarded period” that ran from January 20, 2020, to July 10, 2023. This generally impacts tax returns for the years 2019, 2020, 2021, and 2022.

Do small businesses qualify for the COVID penalty refund?

Yes. The relief broadly covers individual taxpayers, small businesses, corporations, estates, and trusts that were assessed eligible penalties during the defined pandemic timeline.

What happens if the Department of Justice wins the Kwong appeal?

If the government wins the appeal and the higher courts overturn the Kwong decision, the IRS will not be required to issue the penalty refunds, and your protective claim will simply be closed with no payout.

How long does the IRS have to process a protective claim?

The IRS will likely pause processing these specific Kwong-related claims until the judicial appeals process is entirely finished, which could take years. The immediate goal is strictly to meet the July 10, 2026 filing deadline.

Can I still file if I already paid the penalties?

Yes. The protective claim is specifically designed for taxpayers who already paid the penalties and are now asking for that money back as a refund based on the new court ruling.

References

- Taxpayer Advocate Service (IRS) — 2026

- Fast Company — 2026

- Morgan Lewis — 2026

- Aprio — 2026

- Sullivan & Cromwell LLP — 2026

- Moneywise — 2026

- Greenback Tax Services — 2026