Trump Banking Immigration Status Order: Are Accounts Safe?

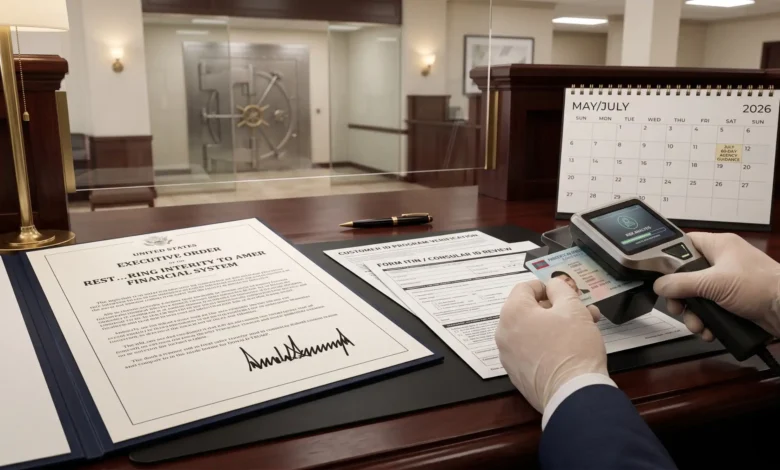

On May 19, 2026, President Trump signed an executive order targeting non-citizen access to the US financial system. This action triggered immediate worry among millions of non-citizens, Individual Taxpayer Identification Number (ITIN) holders, and mixed-status families.

While initial rumors suggested banks would immediately require citizenship proof from all account holders, the final directive takes a different approach. It focuses on internal risk management rather than ordering broad, immediate service cancellations.

This guide breaks down exactly what the new directives mean for your money, looks at when changes take effect, and separates verified facts from viral rumors.

Featured Snippet

The executive order signed on May 19, 2026, does not immediately freeze or cancel bank accounts for non-citizens. Instead, it instructs federal agencies to factor immigration status into risk models. Lenders are not required to run universal citizenship checks on every customer, but ITIN accounts and foreign identification will face tighter screening over the coming months.

Key Takeaways

- Signed on May 19, 2026, the executive order is officially titled “Restoring Integrity to America’s Financial System.”

- The policy does not instantly freeze existing bank accounts or completely ban non-citizens from banking services.

- Wall Street and financial industry groups successfully lobbied against mandatory, universal citizenship checks for all bank customers.

- The order flags Individual Taxpayer Identification Numbers (ITINs)—tax processing numbers used by non-citizens—and foreign consular IDs as markers requiring extra screening.

- Lenders will soon face federal pressure to count potential deportation risks when reviewing loan and mortgage applications.

- Federal regulators have 60 to 90 days to write and introduce the specific new banking rules.

Quick Answer: Confirmed vs. Rumored Matrix

| What Social Media Claims | What the Order Actually Says |

| All banks must check your citizenship tomorrow morning. | Lenders are not ordered to run universal citizenship checks on every customer. |

| Existing bank accounts for non-citizens are being frozen. | No immediate account freezes or sudden service blocks are mandated. |

| ITIN bank accounts are now completely illegal. | ITINs remain valid, but banks will apply stricter risk screening. |

| All mortgages for undocumented immigrants are banned. | Regulators must review loan risks, but no outright ban exists. |

Pro Tip: Do not panic and close your bank accounts based on unverified online videos. No sudden, automatic account shutdowns are legally happening today under this directive.

Common Mistake: Many people assume executive orders change banking laws overnight. In reality, they serve as official directives telling federal departments to design new regulations over several months.

What is the “Restoring Integrity to America’s Financial System” Order?

The formal policy establishes a new framework for how US financial institutions handle risk. It instructs banks to treat a customer’s lack of legal work authorization as an active factor when evaluating credit and financial liabilities.

The White House stated that it wants to limit financial system exposures that come from extending credit lines to the inadmissible and removable population. This means the federal government views non-authorized status as an inherent financial risk.

The Banking Industry’s Input

Before the final text was released, major US banking organizations heavily lobbied the administration. Industry groups argued that forcing universal citizenship checks for every single bank account holder would create massive operational costs and overwhelming paperwork.

Lenders also warned that aggressive, universal bans would push millions of undocumented immigrants completely out of the traditional banking environment. This shift would expand the “unbanked” population—people without bank accounts—making the tracking of cash movements much harder for law enforcement. As a result of this industry pressure, the final order relies on targeted, risk-based compliance rules instead of blanket service blocks.

[The White House Briefing Room]

The 2026 Banking Policy Implementation Timeline

The changes introduced by this directive will roll out in distinct waves rather than all at once. The executive order sets clear deadlines for federal oversight agencies to draft and propose specific changes.

Understanding these deadlines helps consumers track exactly when their local bank might update its account terms.

Key Federal Deadlines

The rollout follows a strict chronological schedule over the next six months:

- The 60-Day Treasury Advisory (July 2026): The Treasury Secretary must issue an official advisory to all US financial institutions. This document will outline specific operational hazards tied to servicing non-work authorized populations.

- The 60-Day CFPB Review (July 2026): The Consumer Financial Protection Bureau (CFPB) must evaluate changes to its “ability-to-repay” rules. This means lenders may soon have to calculate the statistical probability of deportation and subsequent wage loss when grading loan applications.

- The 90-Day Bank Secrecy Act Proposal (August 2026): The Treasury Department must propose formal updates to the Bank Secrecy Act—the primary US anti-money laundering law. These changes aim to strengthen customer due diligence, meaning the identity screening processes used by banks.

- The 180-Day Customer Identification Update (November 2026): Long-term updates to the baseline Customer Identification Program rules are expected to finalize, setting permanent standards for how financial institutions verify foreign identities.

Policy Implementation Summary

- Immediate Status: Your bank accounts are safe today; no immediate freezes or automated account closures are taking place under this directive.

- Next 60 Days: Federal agencies are currently drafting the specific compliance rules and guidelines for local branches.

- Targeted Areas: The upcoming regulations will focus on high-risk transaction patterns, foreign identification cards, and long-term credit lines rather than everyday checking accounts.

- Industry Compliance: Lenders are expected to update their internal identity verification and risk software by late summer 2026.

How the Order Impacts ITIN Accounts and Foreign Consular IDs

The directive brings fresh scrutiny to specific alternative identification documents used across the United States. It explicitly highlights Individual Taxpayer Identification Numbers (ITINs) and foreign consular identification cards as items requiring enhanced due diligence.

Under current Customer Identification Program rules, banks have the flexibility to accept these documents to help non-citizens open accounts. The new order modifies this approach by treating these alternative IDs as potential indicators of elevated financial and regulatory risk. Lenders are expected to build multi-layered verification procedures around these accounts.

This means if you opened an account using a passport or consular card, your bank will likely request secondary proof of address, tax records, or employment verification. The goal is to establish a clearer financial profile rather than allowing basic identification to suffice.

Financial Industry Responses

Compliance experts emphasize that banks are trying to balance federal oversight with operational realities. Financial institutions do not want to lose reliable depositors, but they must protect themselves from regulatory penalties under the Bank Secrecy Act.

“While we continue our review and assessment of the Executive Order, it appears as though the directive aligns with our requests for stakeholder input and time to implement any changes.” — Scott Simpson, President/CEO of America’s Credit Unions

Lenders are moving carefully to avoid accidentally shutting down legitimate accounts held by legal residents or green card holders who happen to use alternative IDs.

Mini Case Study: Automated Account Flagging

Typical scenario example: A small business owner operates a registered service company and regularly makes large, repetitive cash withdrawals to pay off-the-books laborers.

Under the upcoming Treasury guidelines, the bank’s automated compliance software flags the account due to the combination of unverified payroll patterns and cash structuring. The bank pauses the account transactions, not because of the owner’s citizenship, but because the transaction pattern mimics payroll tax evasion under the new risk-based compliance definitions. The owner must then supply official corporate tax documentation to restore full account access.

The Impact on Mortgages and Credit Lines

The most significant operational shift will occur in the US housing and credit markets. The executive order targets the extension of long-term credit to individuals who lack permanent legal status or valid work permits.

The policy instructs the Consumer Financial Protection Bureau (CFPB) to revise its ability-to-repay standards. Lenders will be pressured to factor the statistical possibility of deportation or sudden wage loss directly into loan approval algorithms. If an applicant has a temporary visa or lacks work authorization, software models may flag them as high-risk borrowers. This change makes it much harder to clear basic underwriting requirements.

Current Market Reality

Mortgages for non-citizens lacking a Social Security number are already exceptionally rare in the United States. Major secondary market buyers like Fannie Mae and Freddie Mac maintain rigid insurance standards that disqualify most alternative credit structures.

- Market Scale: A study by the Urban Institute estimated that only between 5,000 and 6,000 mortgages are issued annually to customers using ITINs across the entire United States.

- Loan Availability: Because these loans are already uncommon, the new federal restrictions will primarily affect smaller, specialized niche lenders and community housing portfolios rather than the broader national real estate market.

Mini Case Study: The ITIN Home Loan Process

Typical scenario example: A mixed-status family attempts to buy a suburban home using an ITIN and a 20% down payment. Under the new CFPB guidance, the underwriting team must evaluate the primary earner’s long-term immigration stability.

Because the earner lacks a permanent work authorization card, the bank calculates an elevated risk of income disruption due to potential deportation. To offset this institutional risk, the bank denies the standard fixed-rate loan and instead requires a 35% down payment along with a significantly higher interest rate, pricing the family out of the purchase.

Operational Checklist: What Non-Citizens Should Do Next

You can take proactive steps to safeguard your financial access and reduce the risk of automated account disruptions.

- Verify Document Expiration Dates: Ensure your foreign passport, consular ID, or state-issued driver’s license is completely valid and unexpired. Banks routinely freeze accounts when a primary identity document expires.

- Keep Contact Information Current: Update your physical mailing address, phone number, and email with your financial institution. Banks will mail official compliance notices and identity confirmation requests to the address on file.

- Organize Financial Backups: Maintain clear records of your income, including filed tax returns, W-2 forms, or 1099 records. Having proof of legal income helps satisfy risk reviews if an account is flagged.

- Avoid Unusual Cash Patterns: Minimize repetitive cash deposits or withdrawals that fall just under regulatory reporting thresholds, as these trigger automated anti-money laundering reviews.

- Review Bank Disclosures: Pay close attention to any updated terms of service or privacy disclosures sent by your bank or credit union during the summer of 2026.

[America’s Credit Unions Newsroom]

Conclusion & Next Steps

The executive order signed on May 19, 2026, marks a clear regulatory shift in American banking, but it is not a reason for immediate financial panic. By focusing on targeted risk assessment instead of universal citizenship checks, the policy leaves everyday banking accessible for the vast majority of consumers. The coming months will clarify exactly how local banks interpret these federal mandates.

Three Next Steps

- Review your current bank account registration details to ensure your identification is fully updated.

- Monitor official updates from federal financial watchdogs as the July 2026 regulatory deadlines approach.

- Keep clean, consistent paper trails for all major business transactions and personal wage deposits.

FAQs

Will my bank account be closed immediately because of this executive order?

No. The executive order does not order immediate account closures or automatic freezes for non-citizens. It starts a multi-month process where federal agencies design new risk management guidelines for banks to implement later this year.

Do banks check my immigration status when opening an account in 2026?

Banks are required to verify your identity using official documentation, but the final order did not mandate universal citizenship checks for every customer. Instead, banks use risk-based models to evaluate accounts using alternative identification.

Can I still use an ITIN to open a bank account?

Yes. Individual Taxpayer Identification Numbers remain a legally acceptable form of tax and financial identification. However, accounts opened with an ITIN will face closer operational screening and stricter verification checks moving forward.

What happens to existing ITIN mortgages?

Existing, legally binding mortgage contracts remain valid. However, obtaining a new mortgage with an ITIN will become significantly more difficult as lenders begin incorporating deportation risks into loan approval formulas.

What is the CFPB’s role in the new immigration banking rules?

The Consumer Financial Protection Bureau is directed to update its ability-to-repay rules. This means the agency will guide banks on how to treat potential deportation and subsequent income loss as factors when evaluating credit risk.

What are the specific deadlines for these banking changes?

The order establishes a 60-day deadline (July 2026) for initial Treasury advisories and CFPB reviews, followed by a 90-day deadline (August 2026) for proposed changes to the Bank Secrecy Act.

Can I still use a foreign consular ID card as valid identification?

Many banks still accept consular cards, but the new order flags these documents as potential risk markers. Expect branches to request secondary documentation, such as utility bills or lease agreements, to verify your identity.

How does this order affect small business owners paying workers?

Small businesses making large, irregular cash withdrawals to pay unverified workers face a high risk of automated tracking. Banks will closely monitor payroll patterns to stop tax evasion and compliance violations.

References

- The White House, 2026

- Associated Press, 2026

- Bloomberg , 2026

- TIME, 2026

- America’s Credit Unions, 2026